What Changes Are Coming to Medicare in 2026?

Medicare evolves every year, and 2026 brings the first wave of negotiated Part D drug prices, updated premiums and deductibles, and expanded behavioral‑health and telehealth policies.

In this article, we break down what changed, why it matters, and the smart moves to consider before (and after) open enrollment windows.

Need help reviewing your 2026 options? The agents at Senior Allies can walk you through it. Call 833‑801‑7999 for personalized guidance.

1. Part B Costs: Premiums & Deductible Are Up in 2026

What changed: The standard Part B premium is $202.90/month in 2026, and the annual Part B deductible is $283. This reflects the routine CMS update tied to program costs and projections. If you’re billed directly (or newly starting Part B), expect those figures unless you owe more under IRMAA (Income-Related Monthly Adjustment Amount).

Why it matters: Your premium comes out of your Social Security benefit (if you receive it) or is billed to you. The deductible is the amount you must pay for Part B—covered services before Medicare shares costs—so plan for that early‑year spend if you have scheduled imaging, therapies, or outpatient procedures.

Tip: Review whether your providers accept Medicare assignment. This can help minimize surprise balances after the deductible.

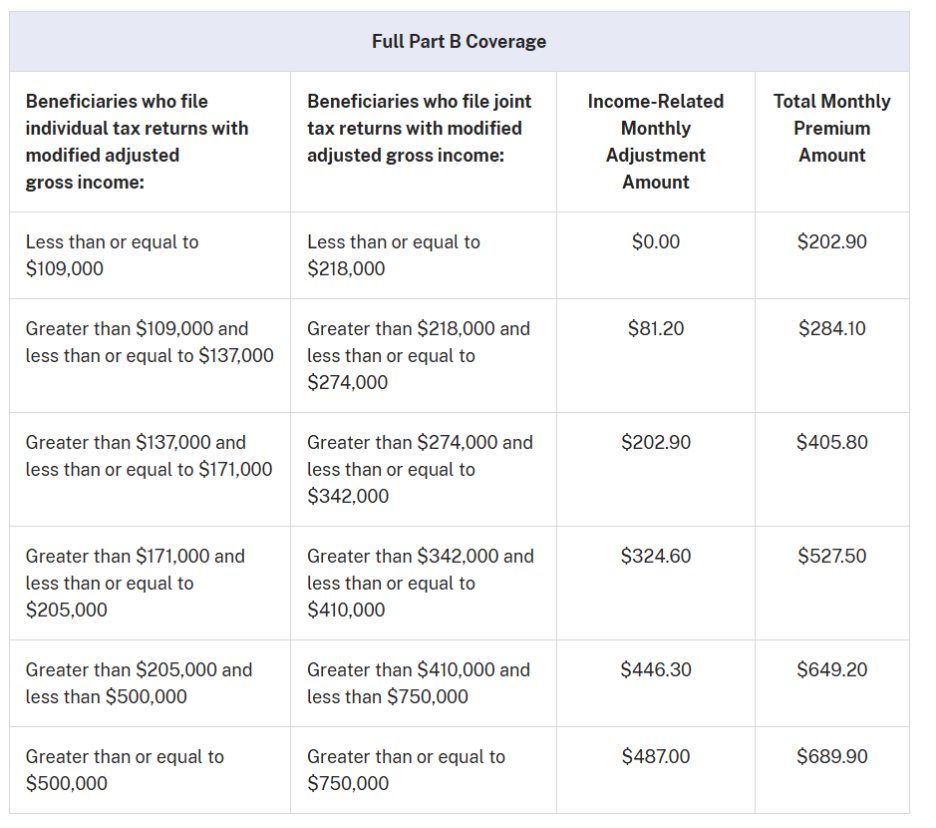

2. IRMAA: High‑income fees adjust as 2026 limits shift

What changed: IRMAA brackets increase in 2026, and the first surcharge tier starts above $109,000 (individual) / $218,000 (joint). If your 2024 tax return (two years prior) shows income above those thresholds, you’ll pay the standard Part B premium plus an income‑related amount. (IRMAA also applies to Part D.)

Why it matters: A year‑to‑year change in your income (retirement, Roth conversions, asset sales) can push you over a threshold. If your income dropped due to a qualifying life event, you can appeal with Social Security and potentially reduce IRMAA. (The bracket table in CMS’s 2026 cost sheet is your reference point.)

3. Part A: Premiums (If You Buy‑In), Deductible & Coinsurance

What changed: Most people still pay $0 for Part A, but if you don’t have enough work quarters and must “buy in,” 2026 premiums are $311/month (30–39 quarters) or $565/month (<30 quarters).

The inpatient hospital deductible is $1,736 per benefit period; inpatient coinsurance is $434/day (days 61–90) and $868/day (lifetime reserve); skilled nursing facility coinsurance is $217/day (days 21–100).

Why it matters: The Part A deductible is per benefit period, not annual; multiple hospitalizations separated by 60+ days can trigger multiple deductibles.

If you anticipate inpatient or skilled nursing facility care, consider whether a Medigap or MA plan structure best fits your risk tolerance.

4. Part D in 2026: Negotiated Prices Begin, $2,100 Cap, and New Design

What changed:

- Negotiated drug prices for the first set of selected Part D drugs took effect Jan 1, 2026. Plans reflect these prices at the pharmacy counter—check your ANOC/EOC or call your plan to see whether your medications are affected.

- The annual out‑of‑pocket (OOP) cap is $2,100 in 2026 (the 2025 cap of $2,000, inflation‑adjusted). Once you reach the cap, you pay $0 for covered Part D drugs for the rest of the year.

- The standard Part D deductible can be up to $615 (plans may set a lower or $0 deductible).

- CMS finalized the Part D redesign: updated cost‑sharing responsibilities for you, plans, manufacturers, and CMS, and a selected‑drug subsidy that coordinates with negotiated drugs.

Why it matters: The cap means high‑cost medication users finally have a predictable ceiling on spending. But premiums and formularies vary widely—so comparing plans (pharmacy networks, prior auth rules, and tiering) remains essential.

Tip: Use your Prescription Payment Plan to spread expected OOP costs into monthly bills instead of big cash payments at the counter (also known as "smoothing"). This continues in 2026 and appears in Medicare’s consumer materials. (No interest/fees; see plan details.)

5. Expanded Behavioral Health Coverage

What changed:

- CMS expanded mental‑health benefits and care modalities:

- Telehealth coverage now includes common services such as depression screening, tobacco‑use cessation counseling, and caregiver training, helping beneficiaries access care without in‑person visits.

- Digital Mental Health Treatment (DMHT) devices are covered, enabling technology‑based interventions under Medicare.

- Suicide‑risk reduction supports like Safety Planning Intervention and post‑discharge follow‑ups are covered.

Why it matters: These changes broaden who can help and how they can help—especially valuable for people with transportation, mobility, or caregiver constraints. The more flexible coverage also supports earlier intervention and continuity of care.

6. Caregiver Training and Support Now Includes Telehealth

What changed: Caregivers can access training through telehealth to better support loved ones at home (e.g., coaching on care plans, communication strategies, and navigating crises). Expanded eligibility rules for marriage & family therapists (MFTs) and mental‑health counselors (MHCs) widen the workforce available to your family.

Why it matters: Caregivers are often the “hidden” part of the care team. Easier access to training and counseling can reduce burnout and improve outcomes—especially following hospitalizations or behavioral‑health episodes.

7. Telehealth Updates: What Can Be Done From Home and What Requires You To Go In

What changed:

- Starting January 31, 2026, there’s an annual in‑person visit requirement for at‑home behavioral‑health telehealth (exceptions apply for documented barriers).

- CMS also made real‑time audio‑video “direct supervision” for teaching physicians permanent starting in 2026, which supports tele‑behavioral training and team‑based care models.

Why it matters: Expect most of 2026 to feel telehealth‑friendly, but be prepared to schedule that in‑person “check‑in” if you continue at‑home tele‑behavioral care beyond January 30. Your clinician can advise whether an exception applies.

8. Special Enrollment Flexibility for People with Limited Income

What changed: If you’re dually eligible (Medicare & Medicaid) or receive Extra Help (LIS), you can make one plan change per calendar quarter during the first nine months of the year—a longstanding SEP (Special Enrollment Period) that remains in effect and is separate from the MA OEP (Medicare Advantage Open Enrollment Period).

Why it matters: Life and medication needs change. Quarterly SEP flexibility helps low‑income beneficiaries keep coverage aligned with current prescriptions, providers, and budgets without waiting for fall open enrollment.

9. Plan Landscape: Fewer Stand‑Alone PDPs

What changed: The stand‑alone PDP market shrank again for 2026. Analysts tracking CMS landscape files report fewer choices nationally, reflecting the Part D redesign and sponsor consolidation. (Some regions see fewer “$0 deductible” options and shifting premium distributions.) Always review your Annual Notice of Change and compare plans.

Why it matters: Consolidation doesn’t mean worse coverage. It does mean formularies, pharmacy networks, and premiums are moving targets. Even if your 2025 plan served you well, 2026 may present a better fit—especially if you take brand or specialty medications.

Other 2026 Updates Worth Knowing

Advanced Primary Care Management services are now covered to help coordinate complex needs (24/7 team access, care transitions, medication management). Ask your PCP if they offer it.

CT colonography is covered as a colorectal cancer screening option (with defined frequency based on risk), expanding early‑detection choices.

What to Do Next

- List your 2026 meds and preferred pharmacies; run a plan comparison to see total annual drug costs under different PDP/MA‑PD options. (Check for negotiated‑drug impacts.)

- Budget for early‑year costs: the $283 Part B deductible and your Part D deductible (up to $615)—or choose a $0‑deductible plan if the math works out for your meds.

- Consider “smoothing” if you expect high drug costs—manageable monthly billing can prevent early‑year sticker shock.

- Use telehealth strategically through January 30, then schedule required in‑person visits for at‑home behavioral‑health telehealth going forward.

- If you have low income, ask about Extra Help and your quarterly SEP—missing out can be costly.

Conclusion

Those are the major Medicare changes to expect in 2026.

If you have any questions about how these changes will affect you or your coverage, give us a call at 833-801-7999, and our licensed insurance agents will be happy to help you!

Are You Over 65?

The Ultimate Medicare Checklist for Ages 66+ helps you determine what needs to be done after you’re a seasoned Medicare enrollee. Learn how to handle rate increases, price shopping, coverage gaps, and more in this short e-guide.

Download Now

Our team of dedicated, licensed agents can help you as little or as much as you need. Whether it’s answering a few questions about Medicare or creating a comprehensive Medicare Planner with you, we are your Senior Allies.

Email Us Now